Blogs

Part 1: Setting the financial foundation for 2025 success

The countdown to 2025 has begun — are your financials ready? For eCommerce and direct-to-consumer (DTC) businesses, balancing multiple sales channels, paymen...

December 18, 2024

0

min reading time

Blogs

The countdown to 2025 has begun — are your financials ready? For eCommerce and direct-to-consumer (DTC) businesses, balancing multiple sales channels, payment platforms, and tax requirements can feel overwhelming.In this two-part guide, we’ll explore practical steps to clean up your books and prepare your finances for a smooth, successful year ahead.

What makes eCommerce accounting different?

eCommerce businesses often juggle multiple platforms, from online stores to social media sales. Payments might flow through systems like PayPal, Stripe, or digital wallets, adding complexity to every transaction. If your business also includes in-store retail, managing sales across locations can further complicate your accounting and financial reporting.Unlike traditional retail businesses that handle all transactions on one central system, eCommerce and hybrid models (those combining in-store and online sales) must consolidate data from various sources. This added complexity increases the risk of errors in revenue tracking, tax obligations, and financial reporting.For example, if you expand to selling on social media or offer subscription-based products, your accounting process may need to adapt to handle new transaction types and payment frequencies. Similarly, managing in-store sales across multiple locations requires precise tracking of inventory, sales data, and operational costs at each site for accurate financial reporting.

Avoiding common financial pitfalls

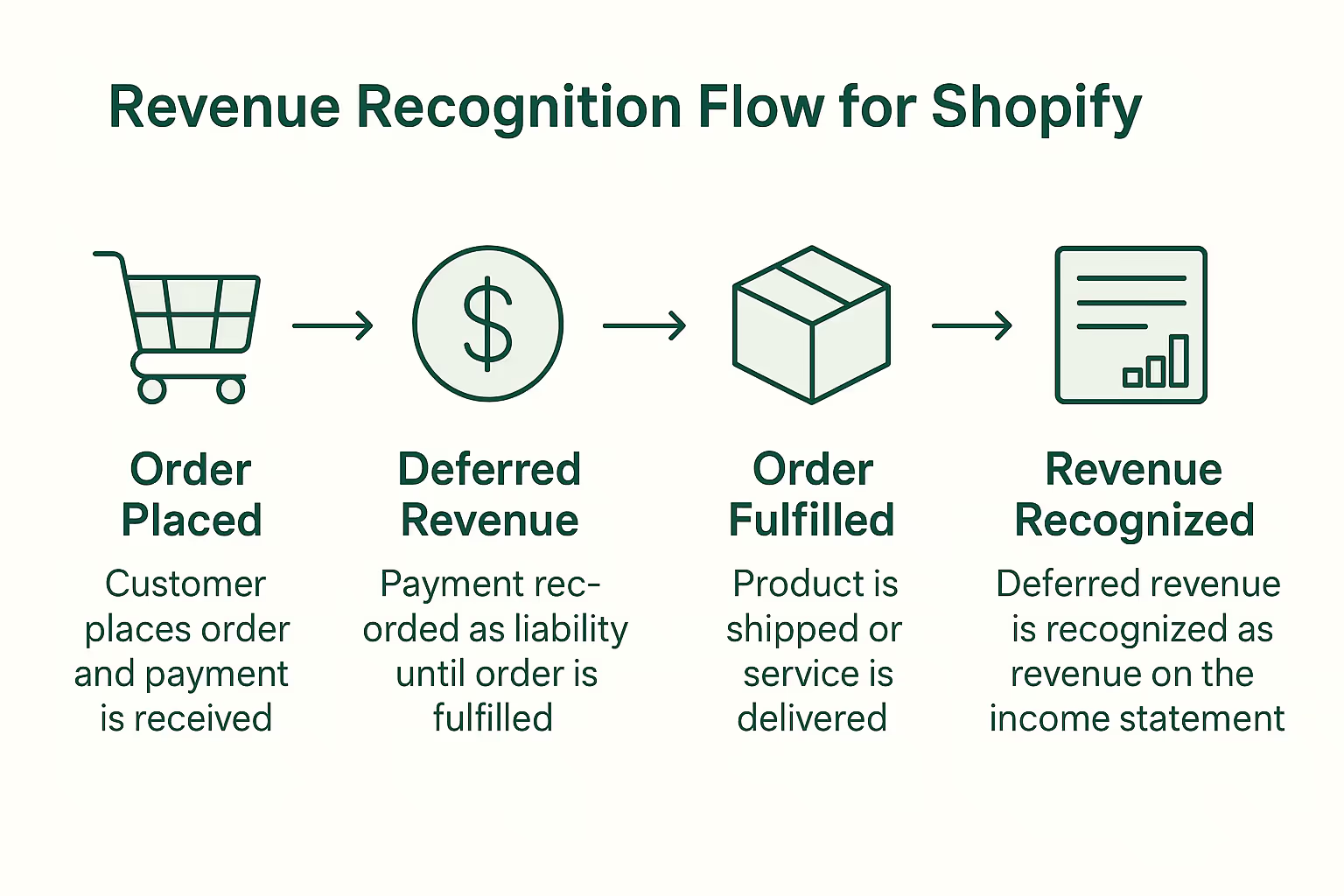

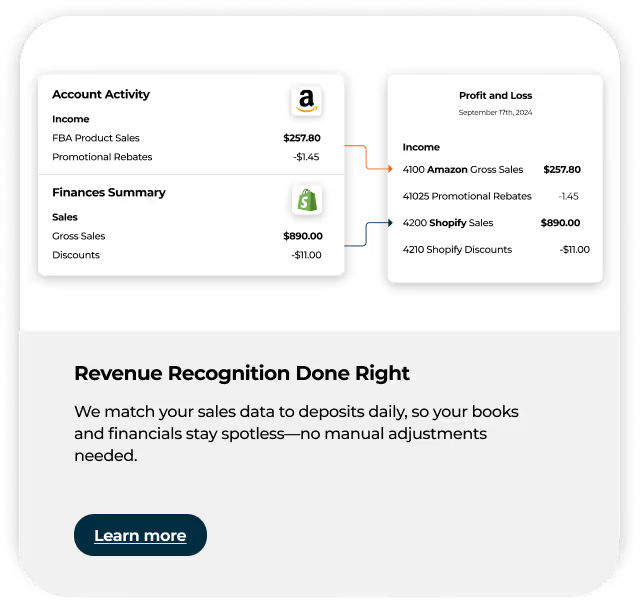

1. Mistakes in revenue recognition

Deposits and pre-orders don’t count as revenue until the product is delivered or the service is performed. Misclassifying these can skew your financial picture and hurt your valuation.

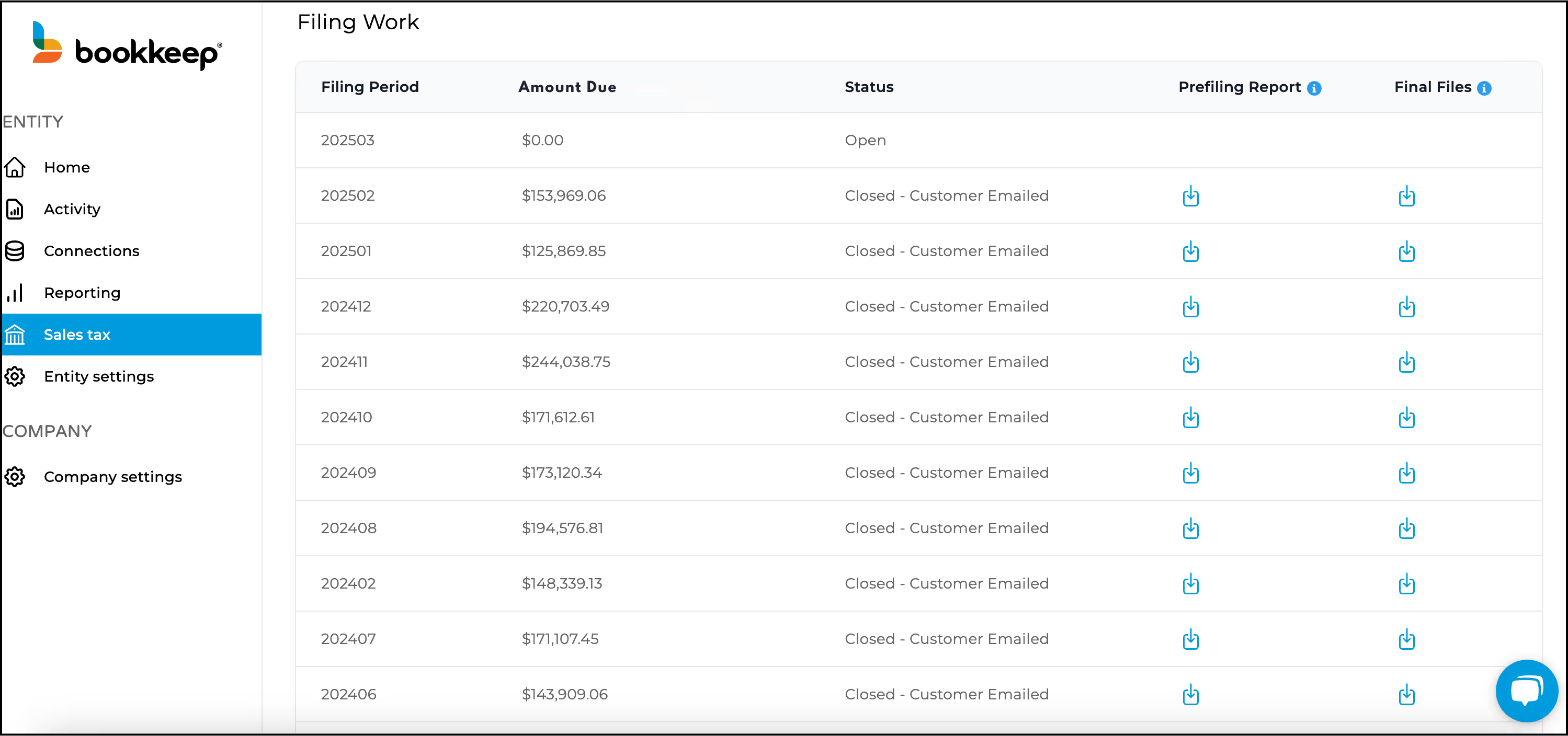

2. Overlooking sales tax obligations

Expanding to new regions brings additional tax responsibilities. Neglecting compliance can lead to fines and penalties.

3. Relying on manual processes

Manual accounting through spreadsheets isn’t scalable. It increases the likelihood of errors and eats up valuable time.

Scaling without sacrificing accuracy

Fast-growing eCommerce businesses often find their accounting processes struggling to keep pace. Here’s how to stay on top:

- Automate wherever possible: Use tools like Bookkeep to sync data across platforms and reduce manual work.

- Consolidate your data: Centralize your financial information for a clear, real-time view of your business performance.

- Monitor trends: Analyze platform and product-level performance to identify opportunities for improvement.

- Keep tabs on taxes: Automate tax tracking and filing to manage complex requirements as you grow.

Building accounting systems for long-term growth

As eCommerce changes, keeping up with new sales channels, payment methods, and regulatory shifts requires scalable systems. Investing in streamlined processes now helps you avoid growing pains later — and positions your business for sustained success.Automating repetitive tasks like revenue reconciliation, tax filing, and expense tracking reduces errors and frees up your team to focus on higher-value activities like strategy and growth.

What’s next?

In Part 2, we’ll discuss advanced strategies like multi-platform reconciliation, detailed reporting, and preparing for audits.Ready to simplify your eCommerce accounting? Learn how Bookkeep can help automate key processes and streamline financial management.Schedule a call or book a demo today.

%201.svg)

You may also be interested some of our other

Blogs

Blogs

April 16, 2026

Bookkeep Launches Integration with Dutchie to Automate Revenue Accounting and Deliver Accurate Financials to Cannabis Retailers

Bookkeep connects your Dutchie POS system to your accounting platform, automating daily journal entries for sales, COGS, refunds, and more — delivering accurate, accrual-based financial records without manual data entry.

Read More

No items found.

Blogs

Blogs

February 12, 2026

Introducing Sales Tax Registrations: Guided Sales Tax Registration with Ongoing Filing Support

Bookkeep now guides merchants through state sales tax registrations and then manages ongoing filing and remittance — ensuring accurate, compliant setup from day one.

Read More

No items found.

Blogs

Blogs

February 12, 2026

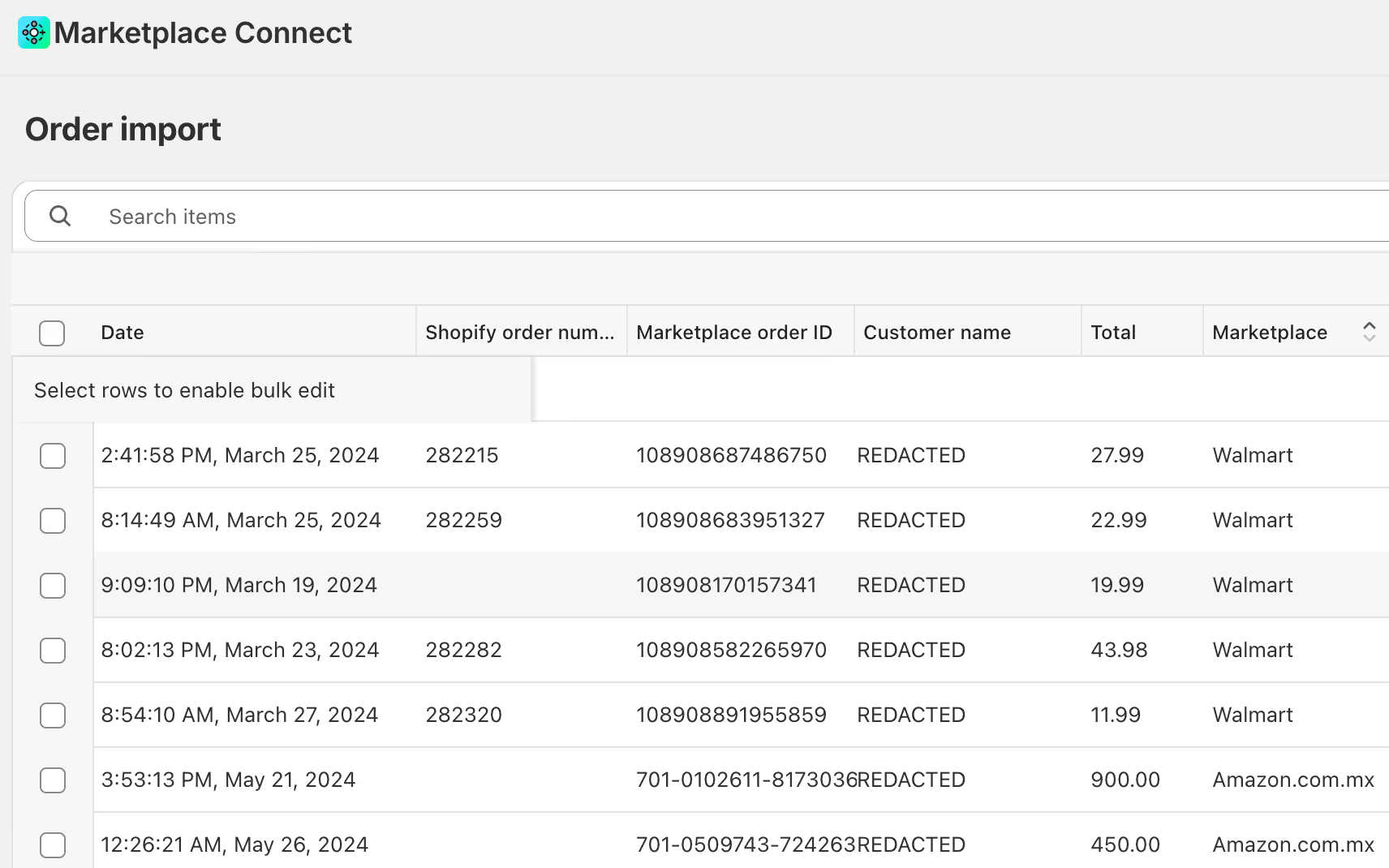

Managed COGS for Walmart: Accurate Gross Margins Without an Inventory System

Walmart sellers can now input product costs directly within Bookkeep to automate COGS posting and improve gross margin reporting — without needing a standalone inventory management system.

Read More

No items found.

Blogs

Blogs

December 17, 2025

2025 Bookkeep Year in Review: Top Product Launches For Financial Clarity

Here's a rundown of all of the major product features we shipped in 2025, all with one goal in mind: helping finance teams reconcile faster, close with confidence, and scale without adding complexity.

Read More

Accounting

Strategy & Growth

Operations

Blogs

Blogs

December 8, 2025

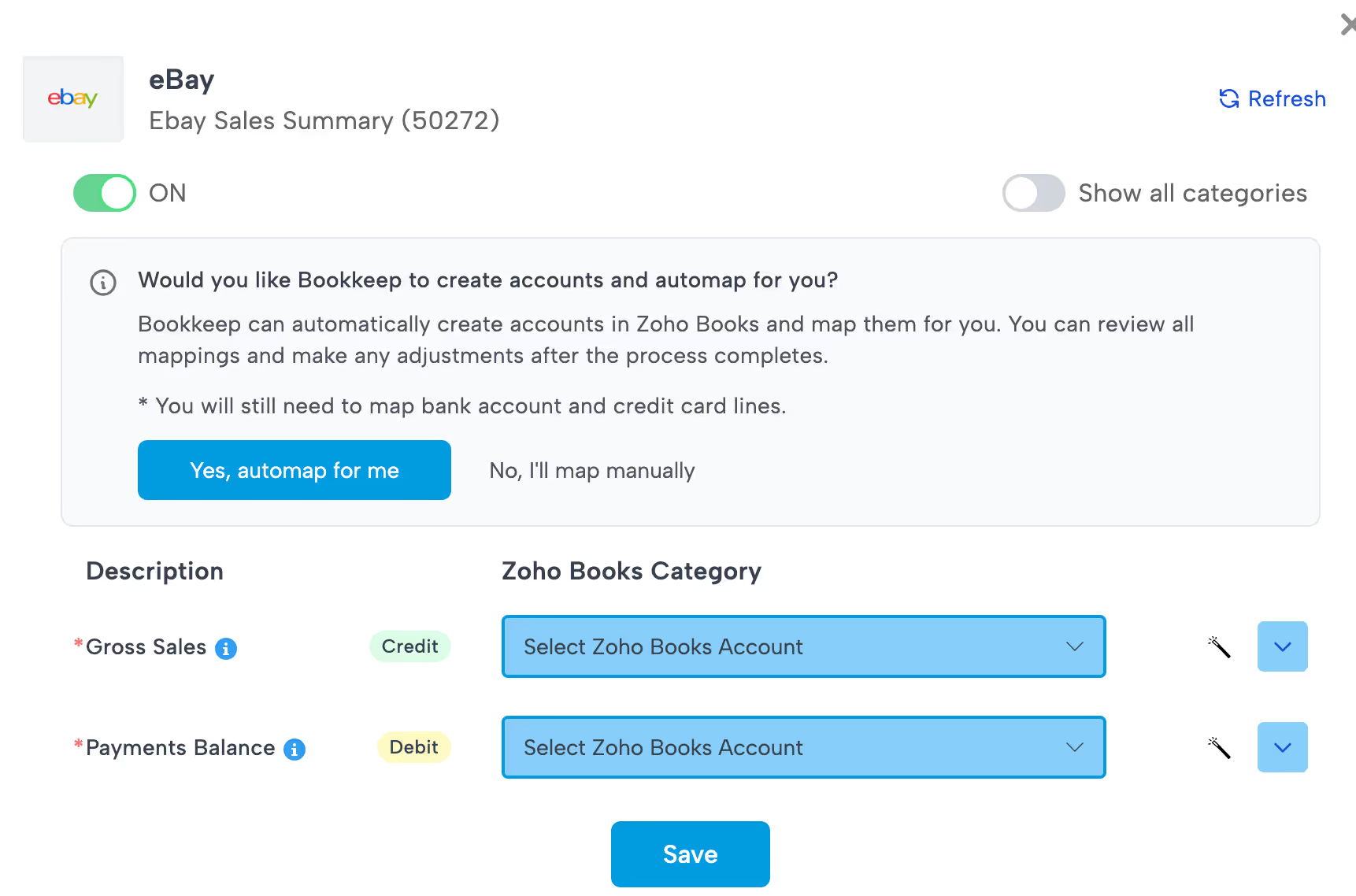

Save Hours on Setup with Bookkeep’s Chart of Accounts Automap Feature

The Chart of Accounts Automap feature from Bookkeep is more than just a convenience — it’s a real productivity and accuracy booster. For any ecommerce brand, retail store or accounting team using Bookkeep (with QuickBooks, Xero, or Zoho Books), this feature removes one of the biggest setup pains: manually building and mapping a clean chart of accounts. With Automap, you get a faster, more consistent path to fully automated, daily bookkeeping.

Read More

Accounting

Operations

Blogs

Blogs

July 14, 2025

Why Shopify Retailers Need Agencies to Migrate and Optimize Their Shopify POS Setup

For brick-and-mortar retailers making the leap to Shopify POS, the transition is about much more than just swapping out cash registers. It’s a strategic shif...

Read More

Operations

Strategy & Growth

Blogs

Blogs

July 8, 2025

Why Specialized Accounting Firms Are Winning Shopify and Ecommerce Clients

Shopify accounting is a category of its own. Firms that specialize—and automate with Bookkeep—are scaling faster, serving better, and standing out. As an acc...

Read More

Accounting

Strategy & Growth

Industry Insights

Blogs

Blogs

June 30, 2025

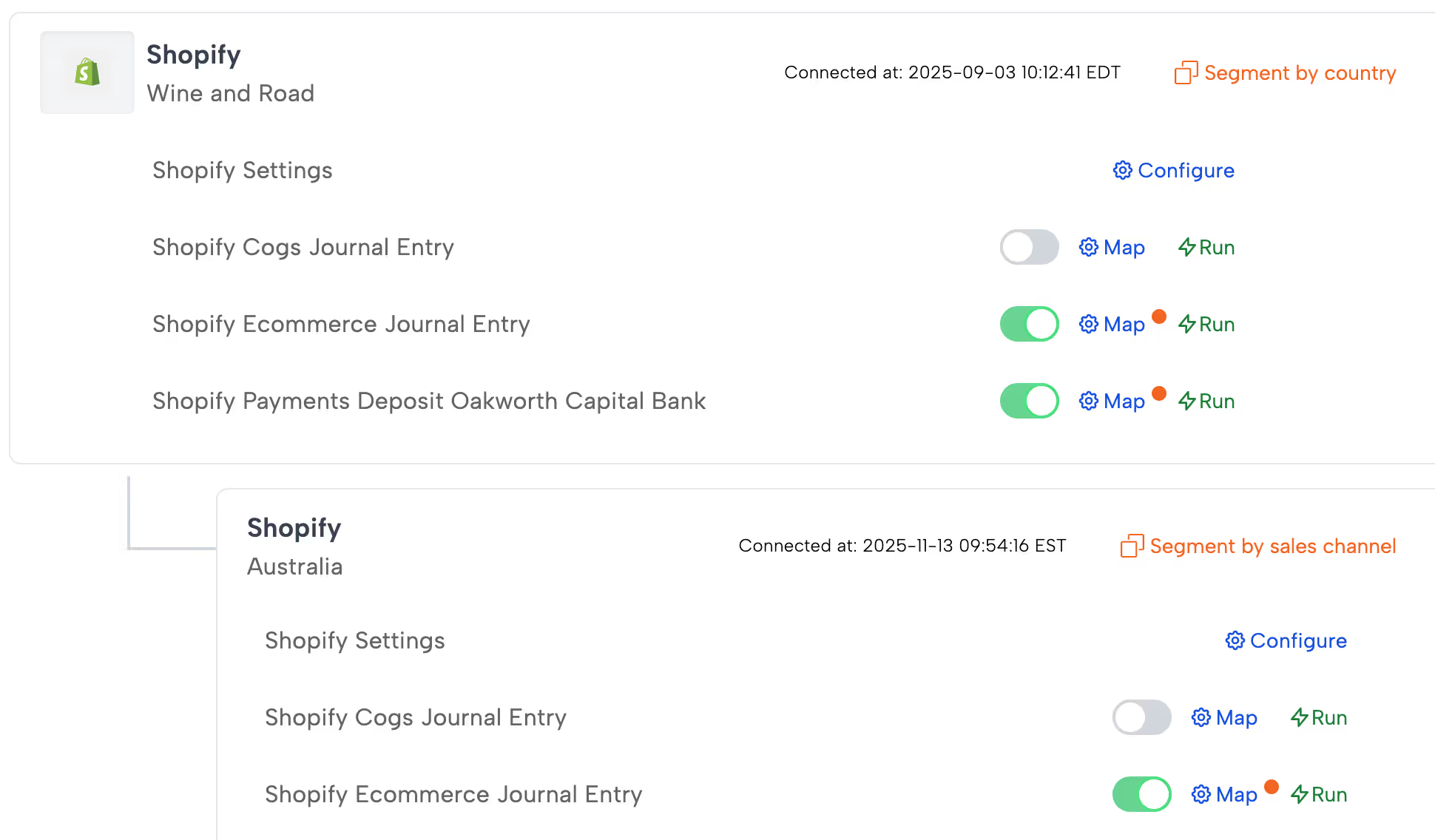

June Product Updates — Smarter Shopify Setup, Flexible Square Reporting, and Zoho Vendor Mapping

At Bookkeep, we’re constantly evolving our platform to align more closely with how ecommerce and retail merchants work. This June, we’ve delivered updates th...

Read More

Operations

Customer Success

Accounting

Blogs

Blogs

June 26, 2025

From Fragmentation to Financial Clarity: How Bookkeep Supports Shopify’s Vision for Unified Commerce

Retail is undergoing a seismic shift. As Shopify’s latest report, “Retail’s Digital Transformation: From Integration to Unification,” makes clear, the future...

Read More

Industry Insights

Strategy & Growth

Accounting

Blogs

Blogs

June 17, 2025

The Ultimate Shopify Agency Technology Stack: What Multi-Million Dollar Brands Really Need to Scale

As Shopify merchants grow past seven figures in revenue, their needs go far beyond a sleek storefront. They’re managing complex operations—across ecommerce, ...

Read More

Strategy & Growth

Operations

Industry Insights

Blogs

Blogs

June 12, 2025

Revenue Recognition Best Practices for Shopify Brands: Stay Compliant & Confident

For fast-growing Shopify brands, understanding when and how to recognize revenue is more than an accounting technicality—it’s essential for compliance, cash ...

Read More

Accounting

Compliance & Legal

Industry Insights

Blogs

Blogs

June 5, 2025

Meet Our Trusted Shopify Agency Partners: Powering Financial Clarity for Merchants

At Bookkeep, we believe in empowering Shopify merchants with seamless, accurate accounting automation. But we know financial clarity doesn’t happen in a vacu...

Read More

Customer Success

Strategy & Growth

Blogs

Blogs

May 22, 2025

Bookkeep Recognized by Gartner with Multiple 2025 Awards for Integration Category And More

NEW YORK, NY, UNITED STATES, May 22, 2025 -- We are excited to share that Bookkeep , an accounting automation solution has been recognized with multiple awar...

Read More

Customer Success

Industry Insights

Blogs

Blogs

May 6, 2025

Accounting Automation: The Secret Weapon for Stress-Free Sales Tax Filings in Ecommerce and Retail

For ecommerce and retail brands, managing sales tax isn't just tedious—it’s a growing liability. With sales across multiple states, platforms, and tax jurisd...

Read More

Compliance & Legal

Accounting

Blogs

Blogs

September 18, 2024

Take Control of Your Books: Meet Our New Features for Shopify and Square Accounting Automation

As CFOs and accounting teams know, keeping books clean and accurate for Shopify and Square merchants can be a time-consuming, manual effort. Between reconcil...

Read More

No items found.

Blogs

Blogs

July 15, 2024

How to Avoid Double-Booking Revenues, when Using Shopify (or WooCommerce, or Amazon) and PayPal Together

Shopify and PayPal play so nicely together. Or, do they? The short answer is “Yes, they do”, but the longer more nuanced answer is that companies that use th...

Read More

No items found.

Blogs

Blogs

June 18, 2024

Bookkeep Opens New Office in Victoria, British Columbia To Better Serve Its Growing Canadian Customer Base

Brooklyn, NY (June 18, 2024) – Bookkeep, the leading revenue accounting and sales tax automation platform for unified commerce, today announced plans to open...

Read More

No items found.

Blogs

Blogs

June 15, 2024

Getting Shopify Sales Detail into QuickBooks Online: Best Practices to Strike the Right Balance

It's a given that in order to understand the business and to be able to make good business decisions, the business owner, CFO, or financial advisor needs dat...

Read More

No items found.

Blogs

Blogs

April 3, 2024

Are You Taking Advantage of Accounting Automation in your E-commerce, Retail, or Restaurant Business?

For busy e-commerce, retail and restaurant businesses (and the accounting teams that serve them), e-commerce and point-of-sale (POS) accounting automation is...

Read More

No items found.

Blogs

Blogs

November 6, 2023

Bookkeep Names Accounting Veteran Alison Ball as Vice President of Marketing and Communications

Former Intuit and Liscio Senior Leader Will Drive Strategy to Increase Awareness and Adoption Among Accountants and Bookkeepers for the Revenue & Sales Tax A...

Read More

No items found.

Blogs

Blogs

June 26, 2023

Bookkeep and Zoho Books Partner to Offer Revenue Automation to Its Growing Community of Accountants and Small Businesses

Additional Integrations with Clover, Toast and MindBody Strengthen Bookkeep’s Position As the Market Leader in Automated Ecommerce Accounting St. Louis, Mo. ...

Read More

No items found.

Blogs

Blogs

April 26, 2023

Specialization: A Solution for Reducing Burnout & Attrition Among Tax & Accounting Professionals

SUMMARY In this column for Thomson Reuters, Jason makes the case for why tax & accounting firms should consider switching to a specialization-focused service...

Read More

No items found.

Blogs

Blogs

March 1, 2023

Bookkeep Introduces New Sales Tax Automation To Provide Retailers Complete Revenue Accounting Services

The Bookkeep and DAVO by Avalara integration will enable clients to automatically set aside sales tax, file and make payments, eliminating tedious manual wor...

Read More

No items found.